The Bullet No.53 Getting Started

The Bullet No.53 Getting Started

TL;DR Adoption growing and cracks in the old system widening

It’s been a month in my new role at Visa and I’m enjoying it immensely. There is much to do, I’m just getting started, and there have already been some moments to make me smile, like getting involved in FIFA Men’s World Cup plans and getting some kudos for my Bitcoin socks. At the same time, there have been many new starts of note in crypto and the wider macroeconomic environment, where some further cracks have started to show. On that theme of starts, it’s time for a few more bullets, but first:

1. The disclaimer

I have to stress that anything I say in these letters is my own opinion and not that of Visa. In addition, nothing here should be taken as financial advice. Yes, I’m taking my compliance training seriously.

2. Starts that grow adoption

There really is too much to cover here and I’m sure to miss something out but pushing adoption just this last month we have:

- Google accepting Bitcoin for cloud services

- Visa (yep my employer) partnering with crypto exchange FTX to offer debit cards in 40 countries

- Subway sandwich shops in Berlin accepting Bitcoin as payment

- McDonalds accepting Bitcoin for payment in Lugano, Switzerland

- An initiative from UK company CoinCorner to bring Bitcoin to the UAE

- Ethereum completes move to Proof of Stake

- Fidelity owned Wise Origin bought over $62M worth of Bitcoin

- Initial code launched from Lightening Labs to issue and transfer assets on Bitcoin, competing with current popular use cases on Ethereum

- Revolut being given permission by the FCA in the UK to provide crypto services

It’s not all roses though

- Decentraland is reported to have only 38 daily active users, nope that’s not millions or thousands, just 38

- Founder of failed crypto project Terra Luna, Do Kwon was tracked down and arrested, after going on the run with users funds

- Similarly, the CEO of crypto lending platform Celsius resigned and stands reportedly accused of stealing funds following declaration of bankruptcy. If that wasn’t bad enough, a data leak also exposed Celsius users personal details, potentially compromising their security

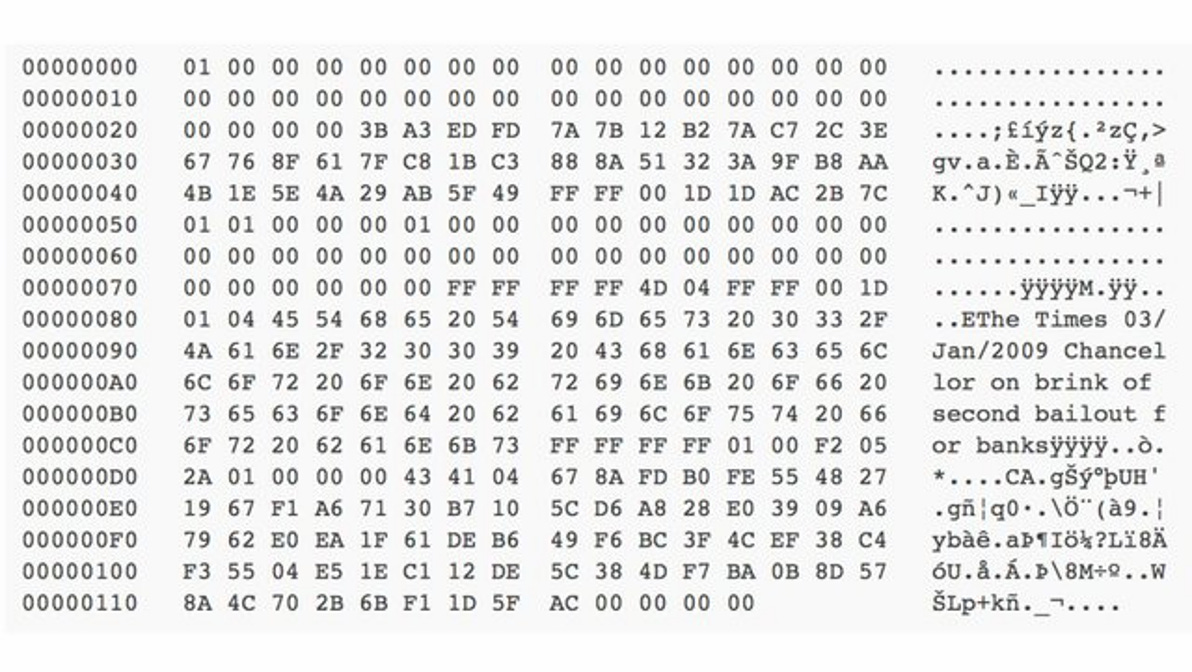

3. The start of Bitcoin

When the Bitcoin blockchain was started in 2009, embedded in the first block of transactions was a headline from the Times that read “Chancellor on brink of second bailout for banks”, in reference to the UK bailout of banks during financial crisis of the time. This neatly sums up the purpose of Bitcoin as the antithesis of the prevailing money system, where new money can be easily created to rescue and reward entities who don’t suffer the consequences of their bad decisions

4. The start of a new financial crisis

13 years later and we had a similar headline in the Financial Times on the 12th October 2022 that read “Bank of England buys gilts again to prevent ‘fire sale’ by pension funds”. What’s happening today is that the government debt market, often referred to as gilts or bonds are being found out for being overextended, as I’ve referred to in previous letters.

The answer from the system again is to simply create more money in order to bail out that problem. However, the background and consequences today are different to 2008, although just as severe, if not more so.

5. Starting at a different point

Back in 2008 we weren’t living in a time of double-digit inflation, whereas now we are. The Bank of England is trying to reduce inflation and prevent default of the UK government debt at the same time, but if they create more money now, the worry is that it will fuel inflation even further. Therefore, the choice is let pension values fall, because many of them invest in government debt, or let inflation run high for longer. Either way you lose.

6. It’s global

There is a lot of attention and focus at the moment on the UK, and perhaps I’m simply more exposed to it since I live here, but this is a global problem. Every major western economy has high unsustainable government debt from Europe to the US and Japan. They’re all facing the same issue, it’s just the UK where this is currently most acute, although arguably other economies are in a much worse position. It’s very easy to blame the current UK government, who’s actions aren’t helping but the underlying problem is the systemic, which has been building since 1970s and our removal from a gold standard base of money.

It’s this situation that Bitcoin was invented for. The benefits of a system that isn’t controlled centrally and punishes poor decision making, instead of bailing it out, becomes more obvious and appealing by the day. It was perhaps always wishful thinking to be able to switch to a Bitcoin standard overnight, without further hardship on populations. The cracks are starting to deepen and something will break soon, but I think the case for Bitcoin will grow stronger as a result. The volatility of the 2020s are just getting started,

Peace, love and Bitcoin.

Rob